Market Briefing: Bottlenecks & Breakouts - How AI Is Rewiring Market Leadership

Jun 29, 2026

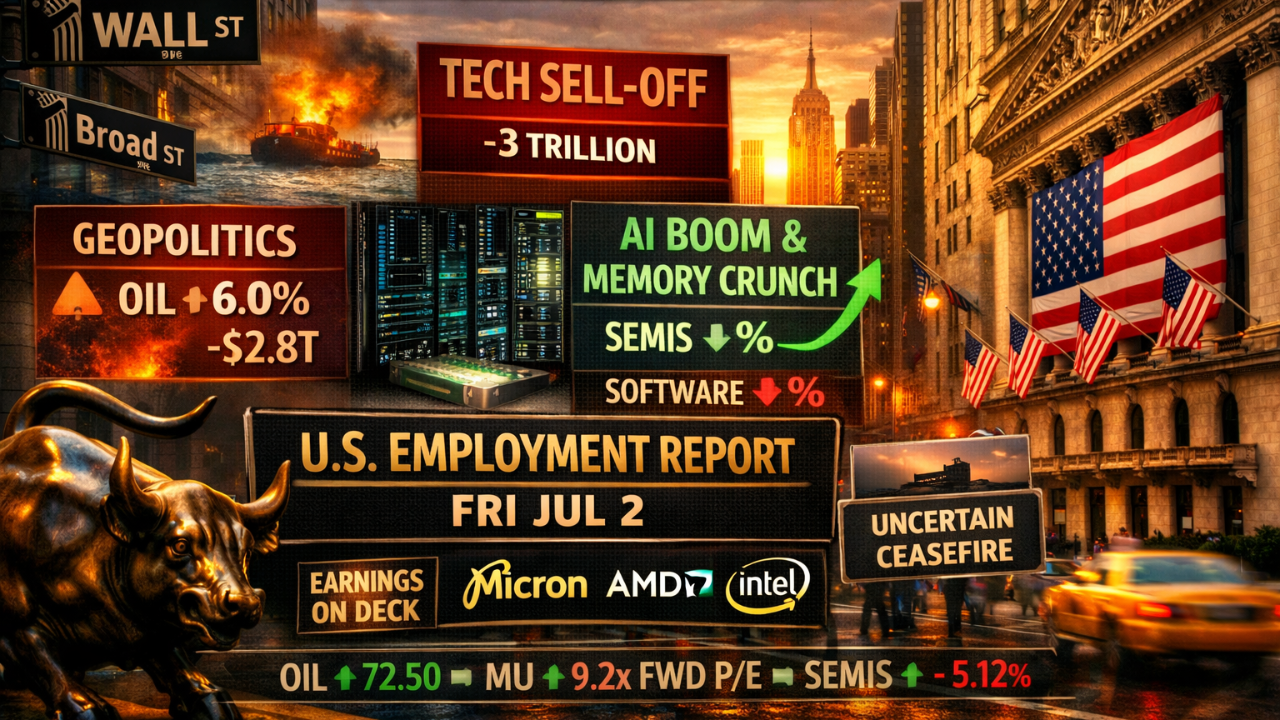

The U.S. market is entering a pivotal stretch where unmatched macro strength, surging AI investment, and massive global inflows collide with a sharp tech correction, rising geopolitical risk in the Strait of Hormuz, and a dramatic power shift inside the semiconductor supply chain. AI capex continues to fuel GDP and reshape corporate profitability, yet bottlenecks, cost inflation, and margin pressure are forcing a rotation away from hyperscalers and software toward upstream semis, led by Micron, now one of the most profitable companies in America. With oil volatility, a fragile ceasefire, and a $3 trillion megacap drawdown setting the backdrop, markets head into July searching for stability, leadership, and clarity ahead of a critical earnings season.

U.S. Macro & Market Dominance

- Foreign investors poured $1.4T into U.S. assets over the past year.

- U.S. equities now represent ~50% of global market cap, far ahead of all other regions.

- Dollar reserve status remains stable across all major metrics (FX volumes, Swift, cross‑border loans, etc.).

- U.S. companies continue to show superior ROE/ROA vs. Europe, Japan, China.

- Structural advantages: 200 years of institutional stability, massive domestic market, abundant resources, pro‑business legal system.

AI Boom Driving GDP & Capex

- AI investment added 0.7-0.8 percentage points to GDP in Q4 2025 and Q1 2026.

- AI equipment spending running 14-16% annualized, strongest since the dot‑com era.

- Hyperscalers expected to invest $1T+ in 2026 on chips, memory, and data‑center buildouts.

- AI demand is now inflationary (chips, electricity, components).

- S&P 500 up 65% over three years; NVDA up 362%.

June Tech Meltdown & Rotation

- Nasdaq down ~6% in June worst month since March 2025.

- Magnificent Seven lost $2.8-$3T in market cap this month.

- Memory‑chip bottlenecks → hyperscaler cost blowouts → margin compression → valuation reset.

- Software de‑rated as investors question AI disruption risk.

- Leadership rotating upstream into semis and memory suppliers.

Geopolitics & Oil Volatility

- U.S. and Iran agreed to halt attacks after weekend strikes in the Persian Gulf.

- Strait of Hormuz remains a live wire; any flare‑up = oil spike + risk‑off.

- WTI +1.3% Sunday, Brent +1%, but both still down ~20% month‑to‑date.

- Markets stabilizing on belief that “peace, however ragged, remains on the table.”

In Summary: U.S. macro dominance remains unmatched with AI capex is still accelerating, but cost inflation is now a headwind. While tech leadership is shifting upstream into semis and memory suppliers, Hyperscalers face margin pressure and software face business‑model risk. Oil + geopolitics remains macro wildcard. July earnings should be critical validation moment for the AI cycle.

Join us TODAY for 1 full year of 25% off July 4th Special

Enter Discount Code: 4THJULY at checkout

(This coupon expires at 11:59p.m July 6th, 2026)

From MyCompass Trading community to you

Want to get our Stocks to Watch Report every trading day? Get a free 7-day trial of the MyCompass Pro membership!